Get to know the IRS, its people and the issues that affect taxpayers

By Andy Keyso

CL-21-12, April 8, 2021

While some other articles for A Closer Look have focused on compliance activities (such as audits or collection actions) that the IRS takes to ensure taxpayers adhere to the federal tax laws, it’s important to remember that the tax law is complex, and even though IRS employees making compliance determinations are bound to apply the tax law fairly to all taxpayers, it’s not unusual for a taxpayer and the IRS to disagree about the proper application of the law to the taxpayer’s personal situation. Where does a taxpayer turn when such a disagreement exists? Must the taxpayer challenge the IRS’s determination in court?

As Chief of the Independent Office of Appeals, I’d like to remind taxpayers that they can have their case reviewed by an Appeals Officer who is independent of the IRS compliance function that made the initial determination in their case. I’m a big believer in a strong appeals function within the IRS. During my 30 years with the Internal Revenue Service, I’ve had the privilege to experience the tax system from a variety of perspectives. I spent seven years auditing and reviewing audits of taxpayers’ income tax returns, and another 18 years in the Office of Chief Counsel interpreting the law and applying it to specific taxpayer situations. I’ve seen firsthand how complex law or unique facts can lead to uncertainty in how the law applies to the taxpayer. I’ve also seen how taxpayers who are unfamiliar with the tax system may be unaware of their right to seek a review of an examination or collection action. Informed by these experiences, I joined the Independent Office of Appeals in 2017, and now lead a group of Appeals employees dedicated to ensuring that taxpayers receive an independent and impartial “second look” at their disputes with the IRS. Read on, and I’ll introduce you to the Independent Office of Appeals and explain how to appeal an IRS determination and what to expect when your case comes to Appeals.

Appeals is an independent function within the IRS, completely separate from the compliance functions responsible for collecting and assessing taxes. Appeals provides an informal forum for taxpayers who disagree with an IRS determination. Our job is to resolve tax disputes without litigation, where possible, consider each case fairly and impartially and improve public confidence in the integrity and efficiency of the IRS.

We do this by listening to taxpayers, understanding both sides (taxpayers and IRS compliance), independently evaluating all arguments and available information and identifying appropriate settlement options. We have an overall staff of approximately 1,240 employees, mostly Appeals Officers and Settlement Officers. An Appeals Officer typically handles matters involving audit-related issues like penalties or additions to tax. For some complex matters, Appeals Officers may work as a team with other Appeals Officers. A Settlement Officer typically handles matters involving collection matters like whether the IRS followed proper procedures when imposing a lien or proposing a levy for unpaid taxes.

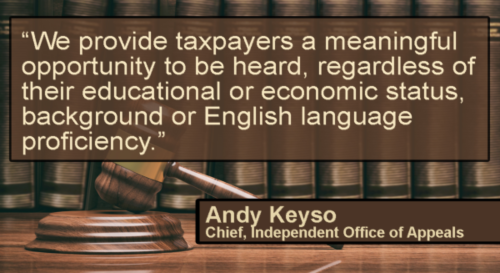

In Appeals, we work with taxpayers informally to settle tax disputes without a formal court hearing and, in most cases, without the need to hire someone to represent them. We provide taxpayers a meaningful opportunity to be heard, regardless of their educational or economic status, background or English language proficiency. In fact, the Taxpayer First Act of 2019 gives taxpayers the right to come to Appeals to dispute most IRS Compliance determinations.

Appeals is unique within tax administration, because we have the authority to compromise the amount of tax owed to resolve a dispute. This means Appeals can offer taxpayers a fair settlement based on the probable outcome if their case were to go to court. We refer to this as evaluating the "hazards of litigation." Here, I should note that not every dispute merits a compromise and some issues do not raise hazards of litigation. Appeals Officers and Settlement Officers are trained to carefully review the facts and law of each case to reach an impartial and fair settlement. You can improve the chance of a favorable settlement by providing as much evidence and supporting documentation as possible with your case. Though not required, taxpayers may have a representative handle their case. Taxpayers who are unable to pay a representative may be eligible for assistance for free through a Low Income Tax Clinic PDF .

Typically, appeal rights become available following a compliance action by IRS that could include an audit, penalty assessment or notice of a collection action. If you receive an IRS notice and your case is eligible for an appeal, the notice will explain your appeal rights. At that point, if you disagree with the IRS determination, you can request an appeal. The next step is to write down, either in a formal protest or simple statement, the issues with which you disagree and why. You can find out more about how to request an appeal and where to send it on IRS.gov. It’s important to remember that you should make your appeal request with the IRS compliance person who worked your case. That employee then will be able to send your appeal request, along with your case file, to Appeals. Taxpayers can also come to appeals after filing a petition in the United States Tax Court to dispute the IRS compliance action.

Once your case arrives in Appeals, we will assign it to an Appeals Officer or Settlement Officer depending on the type of case. Our goal is to have the assigned Appeals employee contact you by mail or telephone within approximately 30 days of receiving your case; however, it is taking longer these days due to pandemic-related delays and other resource constraints. If you have made an Appeals request and feel an unreasonable amount of time has passed, you can read more about how to check on the status of your appeal in the frequently asked questions (FAQs) under what to expect from appeals.

To evaluate your case, the Appeals Officer will fully consider your position and arguments along with the administrative case file from the IRS compliance person who worked your case. You may request to view the non-privileged part of the Compliance file prior to meeting with Appeals. One of the most helpful things you can do is provide all relevant facts, documents and other information supporting your position to the IRS compliance person working your case before it comes to Appeals. If you are unable to locate an important document that might help explain your position, please try to explain the document, why it isn’t available and what steps you took to try to obtain copies, etc. In this way, Appeals will have available all the information necessary to fully review your case. Appeals Officers and Settlement Officers try to resolve cases after holding a taxpayer conference or by correspondence. But, some complex cases may take more than one conference to resolve.

During your appeal, the Appeals Officer or Settlement Officer will discuss with you the facts of your case and how the law applies to these facts. Sometimes the facts and tax law are quite apparent. In other cases, the facts may be difficult to tie down or the law may be subject to multiple interpretations. When faced with this type of uncertainty, the Appeals Officer may review court decisions to see how the courts have ruled in similar situations. As mentioned earlier, Appeals may also consider the "hazards of litigation" or the probable outcome if your case were to go to court.

The scope and nature of our review depends on the type of case. But in all cases, the Appeals Officer or Settlement Officer will listen to your concerns and review any information or comments you present before making a final decision. If your case results in a decision you feel is unfavorable, we will explain the reasons for our decision and any additional options you may have. If you agree to settle your case in Appeals, we may provide you with an agreement form to sign. If you are unable to settle your case in Appeals, you may be entitled to dispute the IRS determination in the Tax Court or another Federal court.

The time it takes for Appeals to work your case depends on several factors, including the type of case, the facts of the case, the complexity of the issues, the availability of legal precedents, other legal theories involved and Appeals’ determination of the hazards of litigation. If you have petitioned the Tax Court prior to coming to Appeals, you have a “docketed” case and the time involved will also be affected by dates and timeframes established by the court and beyond Appeals’ ability to control. Cases received directly from a compliance function that have not been petitioned to the Tax Court are referred to as “non-docketed” cases. Recently, for non-docketed examination or collection appeals, the entire process, from the time your case is received in Appeals to the time it is resolved or closed in Appeals, takes on average 7 or 8 months.

In Appeals, we are always focused on improving taxpayers' experience. Improving the taxpayer experience means ensuring all taxpayers have convenient access to a meaningful and timely appeal. To achieve this goal, we are:

In response to the COVID-19 pandemic, Appeals accelerated a number of these initiatives. Appeals employees adapted quickly and admirably to the changed circumstances. I am deeply grateful for their hard work, which allowed us to continue providing top-quality service without interruption.

I am proud of the work we do and heartened by the professionalism and commitment of my Appeals’ colleagues, who, like most Americans, have overcome many personal and professional challenges over the past year. In coming months, we will build on recent improvements and lessons learned from the pandemic to better meet taxpayers' expectations.

The Appeals process is designed to be informal and easy to navigate. Still, I know it can be a little scary to deal with any government organization. Hopefully, Appeals' independence, quality decision-making and streamlined processes continue to encourage taxpayers to invest the time and resources needed to reach settlements with the IRS. And, my hope is this closer look at Appeals will help you better understand how Appeals can help you resolve a tax dispute without litigation.

Andy Keyso

Chief, Independent Office of Appeals